Tech

Outside Broadcast Production: What Has Changed in the Field

TL;DR: Outside broadcast has traditionally meant RF trucks, cabling, and hours of setup. Cloud linked field units and mobile receivers now let crews go live from a truck, a stadium corner, or a moving vehicle in minutes, with far less equipment on site.

Anyone who has stood next to an OB truck during load-in knows the routine: cable runs, line-of-sight checks, a fixed internet connection to source, and a crew large enough to manage all of it. Outside broadcast work has depended on that routine for decades, and for good reason. RF and microwave links deliver low latency and have earned their place in premium sports coverage. What has changed recently is not the need for reliable transmission, it is how many different ways a crew now has to get there.

Why has on-site production started replacing some RF setups?

RF and microwave systems require line-of-sight and pre-planned frequencies, both of which get harder to secure at crowded venues. A newer class of on-site production tools takes a different approach: a portable field unit at the camera position, paired with a mobile receiver back at the truck, connected over bonded wireless links instead of cable or a fixed line. That swap removes the two most time-consuming parts of setup, sourcing a stable internet connection and running physical cable, and it means camera positions that were previously ruled out by terrain or access can now be used.

Does this replace the truck entirely?

Not for every production. RF and microwave still win on raw latency where a fixed line of sight is available and reliable, which is why they remain standard for some cycling, motorsport, and golf coverage. What on-site production tools add is optionality: a wireless camera in the stands, a position deep inside a stadium where RF struggles, or a last-minute angle that would have been too costly to cable in. The truck stays the hub; the constraint on where a camera can physically go loosens.

What happens when there is no truck at all?

That is where remote production comes in. Instead of sending a full production crew and truck to the venue, camera feeds are sent back to a centralized control room, and the director, replay operators, and technical staff never leave the studio. This model has grown fastest in sports where the venue schedule does not justify a full on-site crew for every game, letting one control room support several events across a week instead of one truck per event.

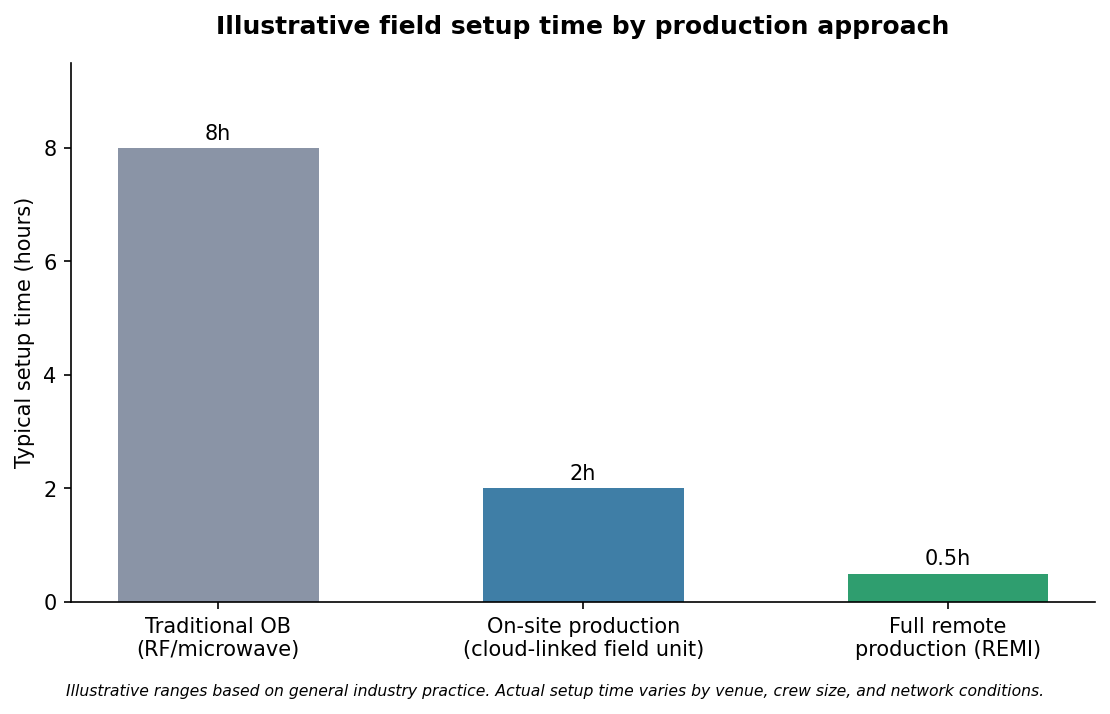

Setup time is where the difference between these three approaches shows up most clearly.

Illustrative field setup time by production approach. Ranges based on general industry practice; actual setup time varies by venue, crew size, and network conditions.

Is one approach simply better than the others?

Not in any absolute sense. A championship motor race with a fixed camera plan and guaranteed line of sight still favors RF. A weekly regional sports broadcast with a tight budget and a need for extra angles is a much better fit for on-site or remote tools. The honest answer is that most serious broadcast operations now run some blend of the three, choosing per event rather than committing to one method for everything.

What should a production team weigh before choosing?

Three questions tend to decide it: how much lead time exists before the event, whether a fixed internet connection can realistically be sourced at the venue, and how many angles the story actually needs versus how many the current setup can afford. Outside broadcast has always been a cost and complexity trade-off. What has shifted is that a wireless, cloud linked alternative now exists at nearly every point on that trade-off curve, not just at the high end.

None of these tools eliminate the judgment calls that come with live production. What they have done is widen the range of venues, angles, and budgets where a genuinely professional broadcast is possible.

Frequently Asked Questions

What is outside broadcast production?

Outside broadcast refers to producing and transmitting a live video program from a location outside a fixed studio, traditionally using RF or microwave links back to a production truck or control room.

How is on-site production different from traditional OB?

On-site production replaces cable and fixed internet dependency with bonded wireless field units and a mobile receiver, cutting setup time while keeping camera positions physically on location.

What is remote production (REMI)?

Remote production sends camera feeds from a venue back to a centralized control room, so the core production crew and equipment stay off site while still delivering a fully produced broadcast.

Public safety agencies, critical infrastructure operators and border security programs have all been quietly rebuilding their video systems around the same idea: cameras that can flag what matters instead of simply recording it. That shift, from passive footage to intelligent video surveillance, is not a marketing trend. The market data behind it, and the operational pressures driving it, tell a fairly clear story about where security video is headed.

The market is scaling faster than most people realize

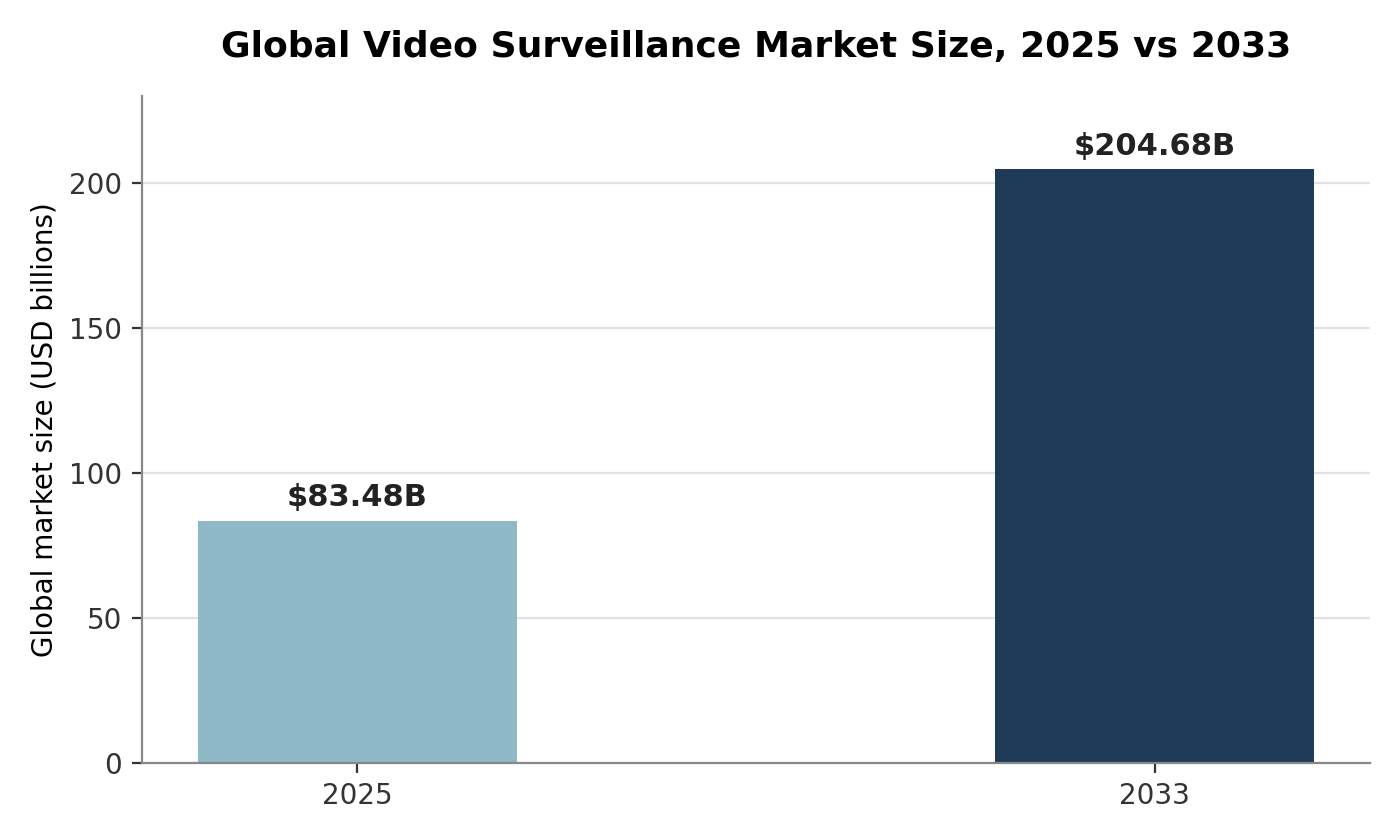

According to Grand View Research, the global video surveillance market was valued at approximately 83.48 billion US dollars in 2025 and is projected to reach 204.68 billion dollars by 2033, a compound annual growth rate of about 11.7 percent. That growth is not evenly distributed. IP based systems already account for more than half of global market revenue, and AI powered analytics, rather than raw camera counts, is increasingly cited by analysts as the segment driving the next phase of expansion. Separately, the broader homeland security market, which includes surveillance alongside border, aviation and critical infrastructure security, is forecast to grow from roughly 716 billion dollars in 2026 toward over a trillion dollars by 2033. Video is a comparatively small slice of that total budget, but it is one of the fastest growing pieces of it.

Why cameras alone are no longer enough

A single operator monitoring dozens of camera feeds cannot realistically watch all of them at once, and fatigue sets in quickly even when they try. That has always been the core limitation of traditional CCTV: the technology captured everything, but a human still had to notice the one frame that mattered. Intelligent video surveillance addresses that limitation by running detection and classification directly against the video feed, so the system itself flags a person entering a restricted zone, a vehicle idling somewhere it should not be, or a gap forming in perimeter coverage, rather than relying on someone catching it live or reviewing hours of footage after the fact.

Where this is showing up first

A few categories of deployment are ahead of the broader curve.

- Critical infrastructure protection. Power, water and transportation facilities are prioritizing systems that can detect intrusion or anomalies automatically, since these sites are often too large and too remote for constant human monitoring to be practical.

- Border and perimeter security. Long stretches of border or perimeter benefit disproportionately from automated detection, since the cost of stationing enough personnel to watch every meter of a fence line around the clock is simply not realistic.

- Homeland security and first responder coordination. Agencies operating under the broader homeland security systems umbrella are integrating video analytics with dispatch and command platforms so that a detection can trigger a response automatically rather than waiting for a phone call.

- Military and defense installations. Bases and forward operating locations increasingly rely on military grade surveillance cameras built to function continuously in harsh conditions, where a conventional commercial camera would fail well before its analytics ever became relevant.

Real time processing is the actual differentiator

The specific technology doing the differentiating is less about camera resolution, which has plateaued at genuinely useful levels for most applications, and more about how quickly a detection reaches a decision maker. Systems that process video on the device itself, rather than streaming everything to a distant server for analysis, cut out the latency and bandwidth cost of that round trip. In a border security or ai homeland security context, that difference between a detection that arrives in under a second and one that arrives after a multi second delay can be the difference between an actionable alert and a missed window entirely.

What the growth curve suggests about the next few years

| Metric | 2025 | 2033 (projected) | CAGR |

| Global video surveillance market | ~$83.5B | ~$204.7B | ~11.7% |

| Global homeland security market | ~$619B (2025) | ~$1,070B (2033) | ~5.9% |

Two things stand out in that comparison. First, video surveillance is growing roughly twice as fast as the broader homeland security budget it sits within, which suggests agencies are actively reallocating spend toward video and analytics rather than simply growing every category proportionally. Second, IP based and AI enabled systems are capturing a disproportionate share of that growth, meaning the money is flowing toward smarter systems rather than simply more cameras.

The practical takeaway

None of this data means every deployment needs the most advanced system available. It does mean that agencies and operators budgeting for the next few years should expect analytics, not additional camera counts, to be where the meaningful capability gains come from. A facility with fewer, smarter cameras that can detect and classify threats in real time is, in most of the scenarios described above, better positioned than one with twice as many cameras and no analytics layer behind them.

IC packaging terminology gets confusing fast, partly because a lot of these acronyms describe overlapping approaches, and partly because the technology has evolved faster than the vocabulary around it. Below are four of the most common points of confusion, and what the terms actually mean once the marketing language is stripped away.

Misconception: Wafer-level packaging is just a smaller version of a normal package

It isn’t smaller so much as structurally different. Traditional packaging processes each die individually after it has already been cut from the wafer. Wafer-level packaging applies the packaging process while the die is still part of the wafer, before singulation, which is what gives it a footprint close to the die size itself rather than simply a tighter version of a conventional package. Fan-out variants take this further by redistributing I/O beyond the die edge, adding routing area without adding package size.

Misconception: System-in-Package and Multi-Chip Module mean the same thing

They’re related but not interchangeable. A system-in-package design combines multiple dies, passive components, and sometimes RF or MEMS elements into a single package that functions as a complete subsystem. A multi-chip module is one way of achieving that, but SiP as a category also covers configurations, like a die plus embedded passives with no separate module substrate, that wouldn’t typically be described as a multi-chip module.

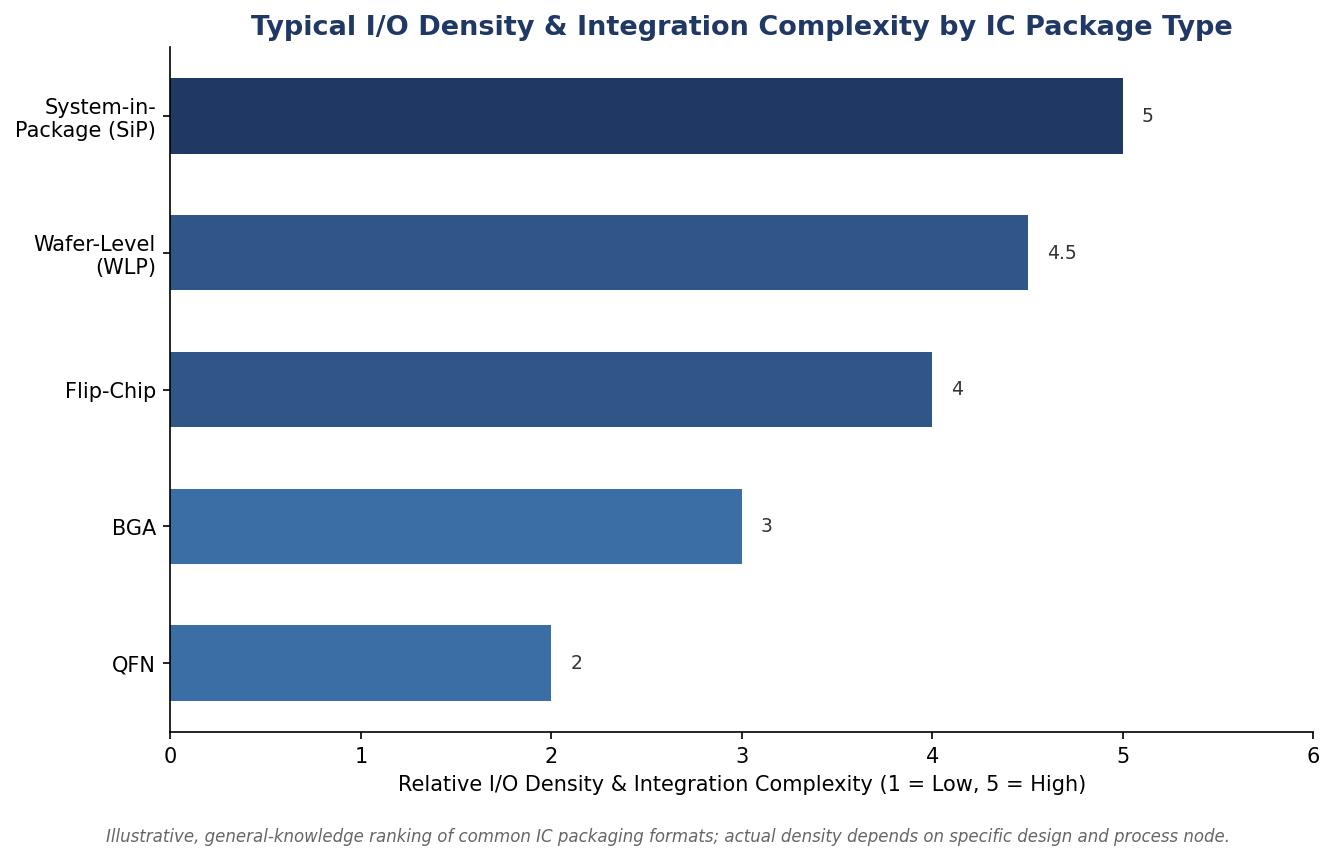

Misconception: QFN and BGA are basically interchangeable

Both are surface-mount package formats, but they solve different problems. The QFN package format uses a lead-frame with exposed pads on the underside instead of protruding leads or a ball grid, giving a smaller footprint and better thermal and electrical performance than older leaded formats, which is why it dominates RF and power-sensitive designs where board space is limited. BGA generally supports a higher pin count for a given footprint, which is why it shows up more in high-pin-count digital and processor packages instead.

Illustrative, general-knowledge ranking of common IC packaging formats; actual density depends on the specific design and process node.

Misconception: Advanced packaging is only relevant for cutting-edge chips

Transistor-level scaling has slowed industry-wide, which has pushed much of the semiconductor industry’s remaining density and performance gains into packaging rather than the die itself. What’s now grouped under advanced packaging technologies (2.5D and 3D stacking, panel-level packaging, fan-out WLP) increasingly shows up in mainstream RF, automotive, and industrial designs, not just flagship mobile processors, because the same footprint and performance pressures exist well outside the leading edge.

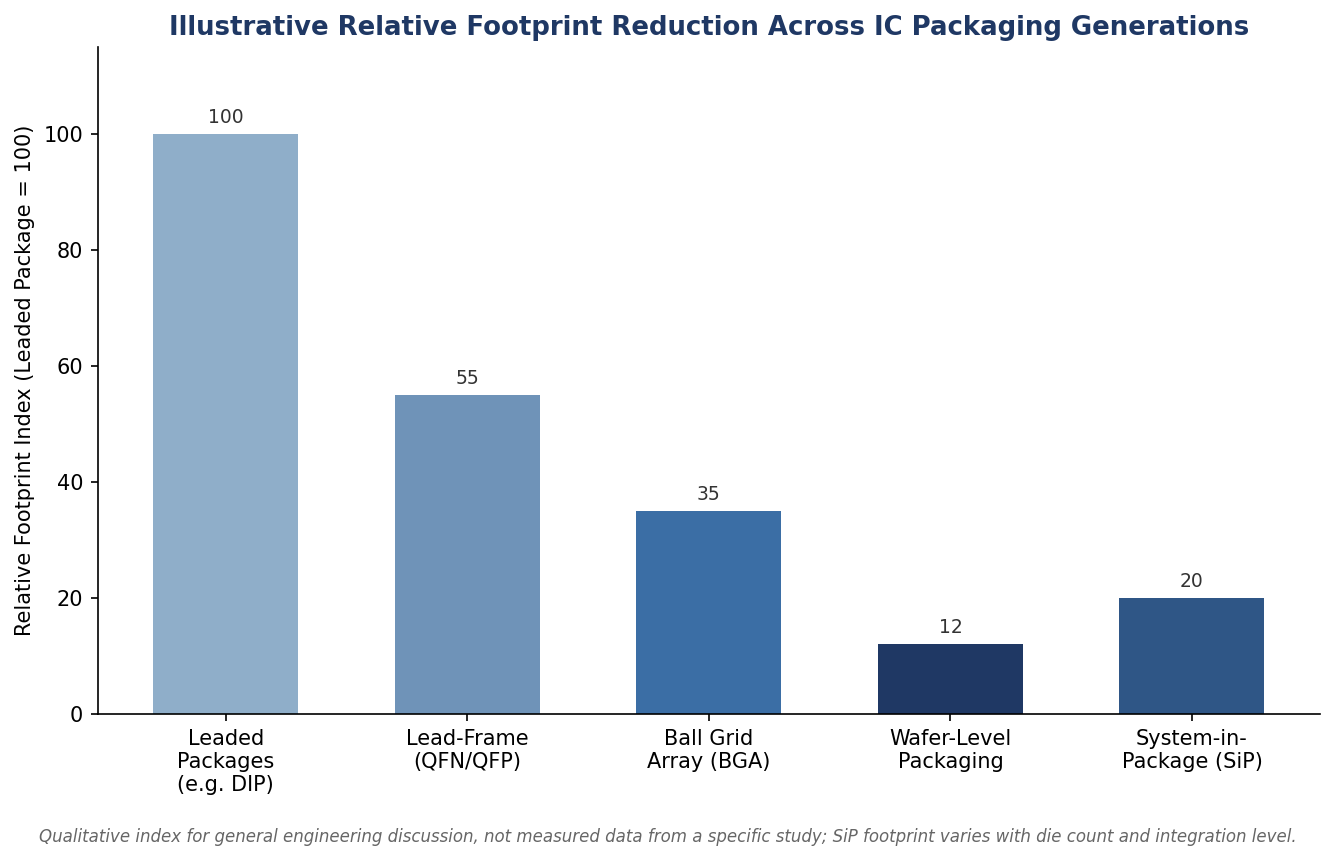

Qualitative footprint index for general engineering discussion, not measured data from a specific study; actual footprint depends on die count and integration level.

The common thread across all four of these confusions is that packaging terms describe trade-offs, not a strict hierarchy from basic to advanced. Choosing the right one depends on which constraint (footprint, I/O count, thermal performance, or integration level) actually matters for a given design.

Frequently Asked Questions

What is the difference between wafer-level packaging and traditional IC packaging?

Wafer-level packaging applies the packaging process while dies are still part of the wafer, before singulation, while traditional packaging processes each die individually after it has been cut from the wafer, generally resulting in a larger final footprint.

What is a System-in-Package (SiP)?

A System-in-Package combines multiple dies, passive components, and sometimes RF or MEMS elements into a single package, so it functions as a complete subsystem rather than a single chip.

Why is QFN packaging common in RF and power-sensitive designs?

QFN packages use a lead-frame with exposed pads on the underside instead of protruding leads, which gives a smaller footprint along with better thermal and electrical performance than older leaded package types.

The long-term commercialization of complex software frameworks cannot rely on financial support alone. Emerging technology segments—ranging from cloud-native software layers to hardware-integrated medical instruments—face distinct operational constraints that defy uniform generalist strategies. Startups navigating the long validation timelines of clinical certifications or the severe code-hardening requirements of critical infrastructure defenses must align with specialized capital networks. If an early-growth company partners with generalist finance groups that lack deep industry insights, it faces significant risks of structural misalignment, missed validation deadlines, and premature failure within competitive international supply chains.

To minimize these market integration risks, institutional innovation pipelines are deploying a specialized, target-grouped enterprise software venture capital framework. Rather than spreading generalist funds thinly across unconnected industries, specialized models isolate individual investments within specific, highly technical verticals. This comprehensive analysis evaluates the structural scaling mechanics across high-barrier domains, outlines why cross-industry groupings require distinct advisory protocols, and details how targeted vertical incubation pathways insulate tech firms from broader macroeconomic market shifts.

Vertical Customization Across Specialized SaaS Platforms

Modern business systems are moving away from horizontal, general-purpose applications in favor of highly specialized, vertical-specific software solutions. Startups developing deep algorithmic tools for complex workflows, such as financial audit automation or high-performance data pipeline monitoring, require specialized infrastructure support from day one. These companies face unique go-to-market challenges, including complex technical evaluations and specialized data localization regulations.

Partnering with a specialized software venture capital firm portfolio structure tailored for these exact parameters resolves these structural challenges. By utilizing deep engineering benchmarks, dedicated investment networks accelerate the transition from initial deployment to predictable enterprise scale. This targeted alignment enables scaling software groups to clear technical review hurdles smoothly, helping them capture market share in competitive enterprise sectors.

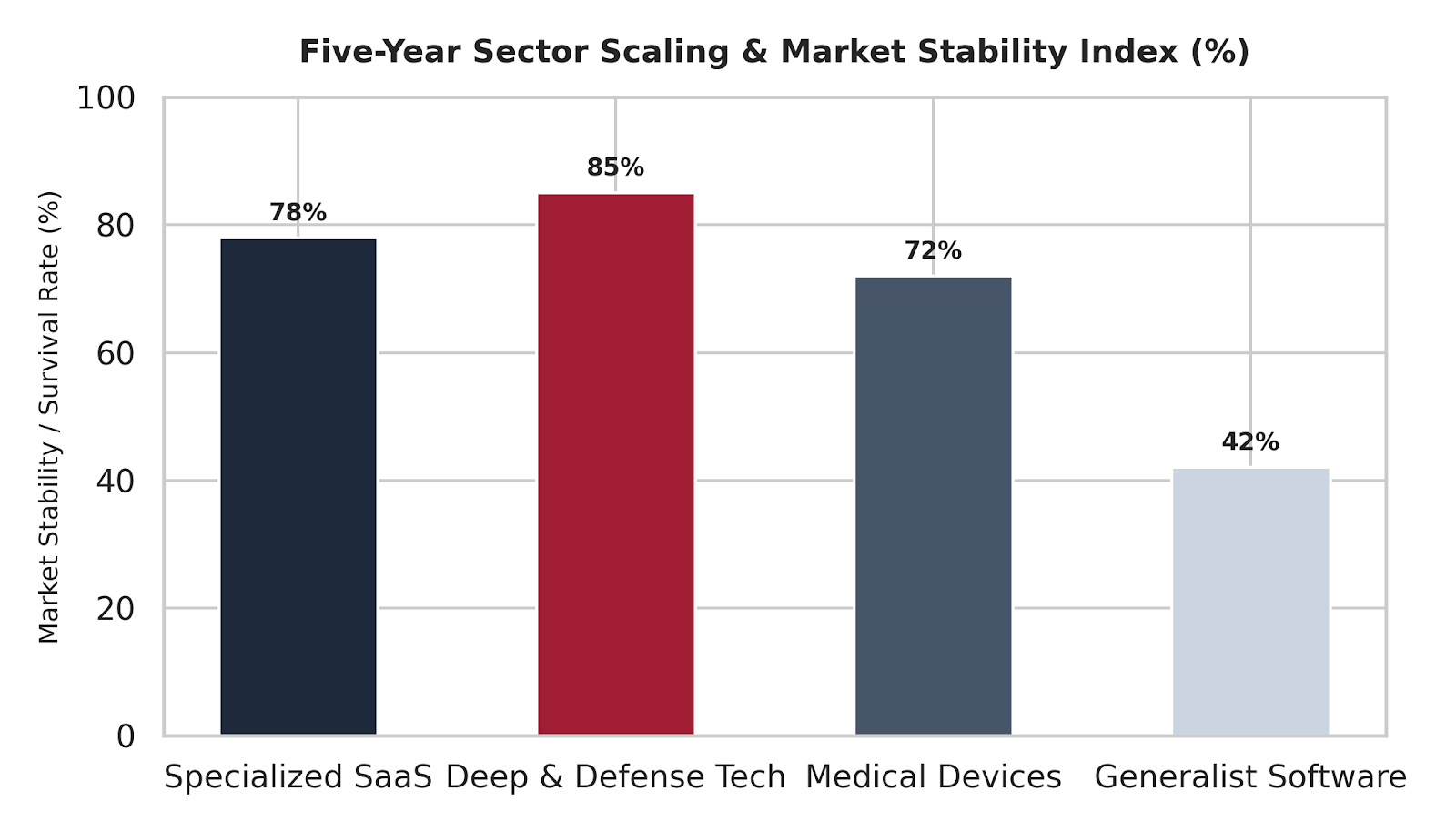

Comparative Performance Metrics: Sector Stability and Scaling Success

Market evidence confirms that startups backed by specialized capital pools achieve substantially higher five-year survival and scaling rates than those relying on generalist finance networks. When investment groups apply deep domain expertise to high-barrier technological verticals, portfolio companies navigate complex regulatory frameworks and commercial onboarding tracks far more efficiently.

The chart below outlines the five-year operational stability index across primary specialized technical segments compared to generalist market alternatives:

Five-Year Sector Scaling & Market Stability Index Breakdown:

Deep & Defense Tech: 85%

Specialized SaaS: 78%

Medical Devices: 72%

Generalist Software: 42%

Specialized Navigation in Medical Device and Deep Tech Sectors

The operational demands of healthcare and engineering technology require highly specialized, domain-specific investment approaches. Developing complex hardware-software configurations requires navigating strict validation tracks, including exhaustive clinical trials and stringent data-security reviews. For instance, a startup pioneering advanced medical diagnostic tools faces long, complex development cycles that standard software investors are rarely equipped to evaluate.

To manage these intense validation demands, sophisticated investment strategies utilize dedicated medical device venture capital support pipelines. These groups combine regulatory advisory teams with deep engineering networks to guide products smoothly from prototype to clinical validation. This specialized model ensures absolute alignment between technical code structures and complex regulatory mandates, transforming early-stage technology into a stable driver of long-term commercial growth.

Conclusion

Securing sustainable global market share in highly technical software and hardware spaces requires a deliberate, domain-specific approach to venture financing. Relying on generalist capital loops introduces significant regulatory alignment risks and unpredictable development timelines. Utilizing a targeted, vertically grouped investment framework ensures that scaling companies possess the capital stability, technical insight, and enterprise access needed to dominate complex markets. As global data security regulations and corporate validation standards continue to tighten, aligning with specialized, expert-backed cybersecurity venture capital structures remains an essential prerequisite for scalable technological expansion.

The Data Behind the Rise of Intelligent Video Surveillance in Public Safety

IC Packaging Terminology Explained: What WLP, SiP, and QFN Actually Mean

Outside Broadcast Production: What Has Changed in the Field

-

Business Solutions2 years ago

Business Solutions2 years agoLive Video Broadcasting with Bonded Transmission Technology

-

Business Solutions1 year ago

Business Solutions1 year agoThe Future of Healthcare SMS and RCS Messaging

-

Business Solutions2 years ago

Business Solutions2 years ago2-Way Texting Solutions from Company Message Services

-

Business Solutions2 years ago

Business Solutions2 years agoCommunication with Analog to Fiber Converters & RF Link Budgets

-

DSRC Communication1 year ago

DSRC Communication1 year agoThe Crossroads of Connectivity: DSRC vs. C-V2X Technologies in Automotive Communication

-

Electronics3 years ago

AI Modules and Smart Home Chips: Future of Home Automation

-

Business Solutions2 years ago

Business Solutions2 years agoWholesale SMS Platforms with OTP Services

-

Business Solutions1 year ago

Business Solutions1 year agoChoosing the Right B2B Digital Marketing Agency: A Guide