Tech

The Data Behind the Rise of Intelligent Video Surveillance in Public Safety

Public safety agencies, critical infrastructure operators and border security programs have all been quietly rebuilding their video systems around the same idea: cameras that can flag what matters instead of simply recording it. That shift, from passive footage to intelligent video surveillance, is not a marketing trend. The market data behind it, and the operational pressures driving it, tell a fairly clear story about where security video is headed.

The market is scaling faster than most people realize

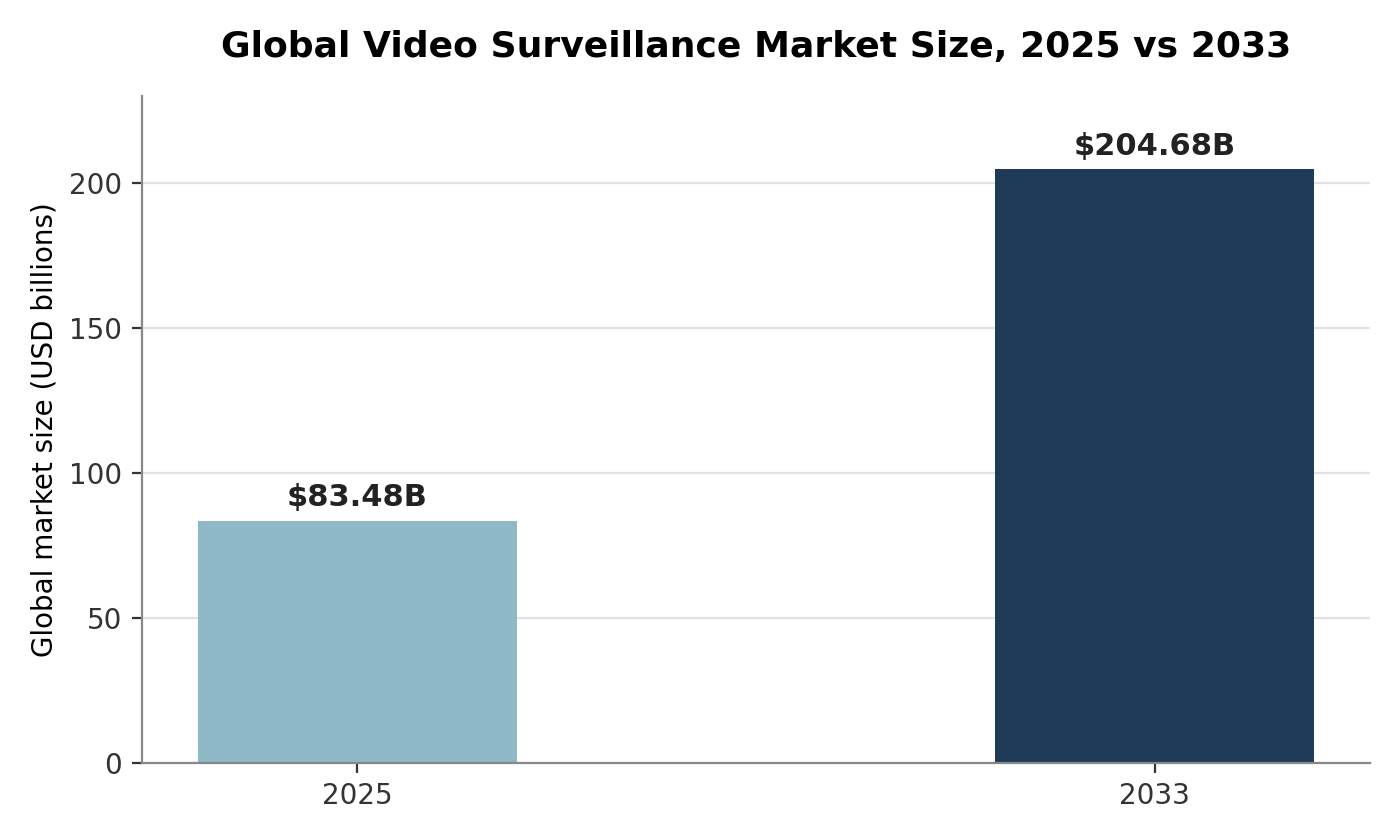

According to Grand View Research, the global video surveillance market was valued at approximately 83.48 billion US dollars in 2025 and is projected to reach 204.68 billion dollars by 2033, a compound annual growth rate of about 11.7 percent. That growth is not evenly distributed. IP based systems already account for more than half of global market revenue, and AI powered analytics, rather than raw camera counts, is increasingly cited by analysts as the segment driving the next phase of expansion. Separately, the broader homeland security market, which includes surveillance alongside border, aviation and critical infrastructure security, is forecast to grow from roughly 716 billion dollars in 2026 toward over a trillion dollars by 2033. Video is a comparatively small slice of that total budget, but it is one of the fastest growing pieces of it.

Why cameras alone are no longer enough

A single operator monitoring dozens of camera feeds cannot realistically watch all of them at once, and fatigue sets in quickly even when they try. That has always been the core limitation of traditional CCTV: the technology captured everything, but a human still had to notice the one frame that mattered. Intelligent video surveillance addresses that limitation by running detection and classification directly against the video feed, so the system itself flags a person entering a restricted zone, a vehicle idling somewhere it should not be, or a gap forming in perimeter coverage, rather than relying on someone catching it live or reviewing hours of footage after the fact.

Where this is showing up first

A few categories of deployment are ahead of the broader curve.

- Critical infrastructure protection. Power, water and transportation facilities are prioritizing systems that can detect intrusion or anomalies automatically, since these sites are often too large and too remote for constant human monitoring to be practical.

- Border and perimeter security. Long stretches of border or perimeter benefit disproportionately from automated detection, since the cost of stationing enough personnel to watch every meter of a fence line around the clock is simply not realistic.

- Homeland security and first responder coordination. Agencies operating under the broader homeland security systems umbrella are integrating video analytics with dispatch and command platforms so that a detection can trigger a response automatically rather than waiting for a phone call.

- Military and defense installations. Bases and forward operating locations increasingly rely on military grade surveillance cameras built to function continuously in harsh conditions, where a conventional commercial camera would fail well before its analytics ever became relevant.

Real time processing is the actual differentiator

The specific technology doing the differentiating is less about camera resolution, which has plateaued at genuinely useful levels for most applications, and more about how quickly a detection reaches a decision maker. Systems that process video on the device itself, rather than streaming everything to a distant server for analysis, cut out the latency and bandwidth cost of that round trip. In a border security or ai homeland security context, that difference between a detection that arrives in under a second and one that arrives after a multi second delay can be the difference between an actionable alert and a missed window entirely.

What the growth curve suggests about the next few years

| Metric | 2025 | 2033 (projected) | CAGR |

| Global video surveillance market | ~$83.5B | ~$204.7B | ~11.7% |

| Global homeland security market | ~$619B (2025) | ~$1,070B (2033) | ~5.9% |

Two things stand out in that comparison. First, video surveillance is growing roughly twice as fast as the broader homeland security budget it sits within, which suggests agencies are actively reallocating spend toward video and analytics rather than simply growing every category proportionally. Second, IP based and AI enabled systems are capturing a disproportionate share of that growth, meaning the money is flowing toward smarter systems rather than simply more cameras.

The practical takeaway

None of this data means every deployment needs the most advanced system available. It does mean that agencies and operators budgeting for the next few years should expect analytics, not additional camera counts, to be where the meaningful capability gains come from. A facility with fewer, smarter cameras that can detect and classify threats in real time is, in most of the scenarios described above, better positioned than one with twice as many cameras and no analytics layer behind them.