Tech

How a Venture Capital Fund Actually Works, From First Close to Exit

When people talk about “venture capital,” they often collapse two different things into one term: the venture capital firm and the venture capital fund it manages. A firm can run several funds at once, at different stages, sectors, or vintages, but each individual fund has its own life cycle, its own investors, and its own clock ticking toward a defined end date. Understanding that structure explains a lot about why VCs behave the way they do, particularly around timelines, follow-on decisions, and exit pressure.

Who actually puts up the money?

Every venture capital fund is built around two groups of participants. Limited partners, typically pension funds, university endowments, insurance companies, family offices, and high-net-worth individuals, supply the bulk of the capital but take no role in day-to-day investment decisions. General partners raise the fund, decide where capital goes, sit on portfolio company boards, and are compensated through a management fee (commonly around 2% of committed capital annually) plus carried interest (commonly around 20% of profits once the fund clears a minimum return threshold, known as the hurdle rate).

Why do funds have a fixed lifespan?

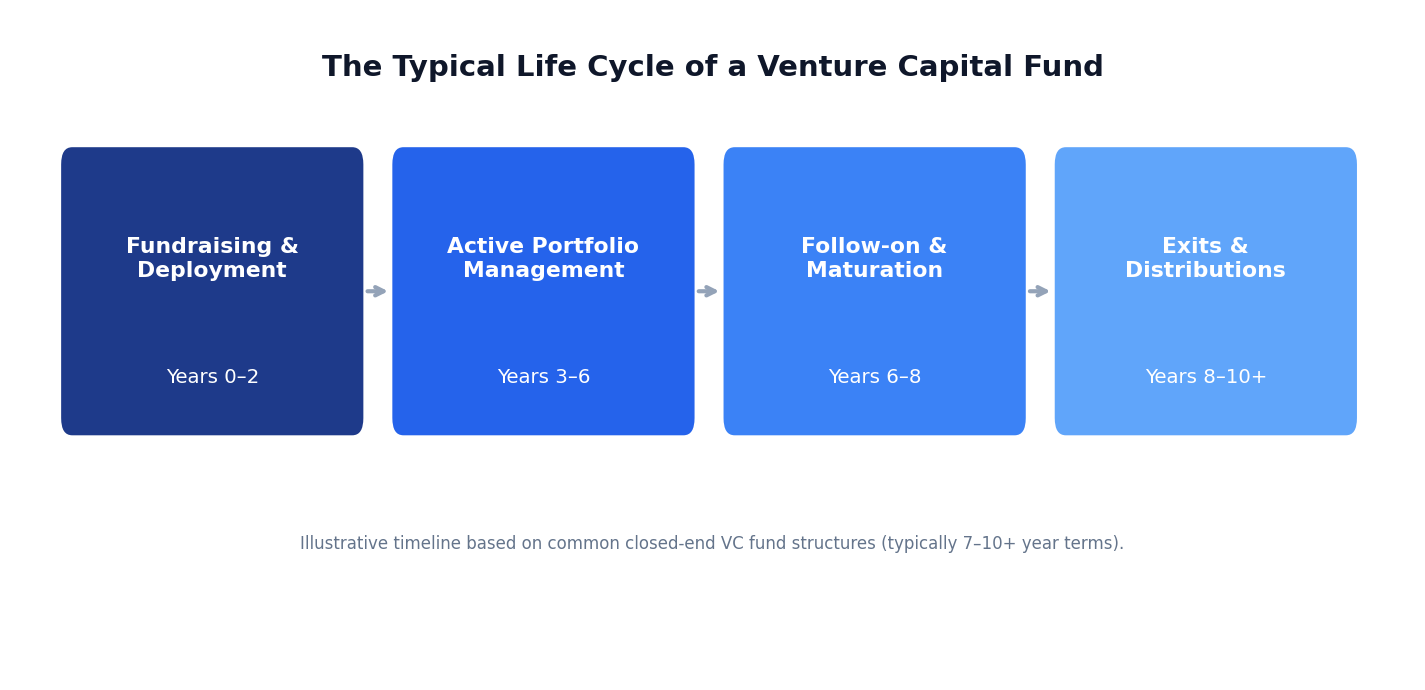

Most venture capital funds are structured as closed-end vehicles with a defined term, typically ten years, sometimes extended a year or two at the general partner’s discretion. That structure is not incidental. LPs commit capital for a fixed period specifically because venture investing requires patience: it can take five to ten years for a startup to reach a meaningful exit, and a fund with no fixed term would have no built-in mechanism for actually returning capital to its investors.

The typical life cycle of a closed-end venture capital fund, from initial deployment through final distributions.

What happens during that ten-year window?

- Years 0–2, Fundraising and deployment: the GP closes commitments from LPs and begins actively sourcing and investing in portfolio companies.

- Years 3–6, Active portfolio management: most new investments happen in this stretch, alongside board support, follow-on decisions, and company-building work.

- Years 6–8, Follow-on and maturation: new investments slow considerably as capital increasingly goes toward defending ownership stakes in the fund’s strongest performers.

- Years 8–10+, Exits and distributions: portfolio companies reach acquisition, IPO, or other liquidity events, and the fund returns capital, plus any profit, back to its LPs.

Why does a small number of investments matter so much?

Venture returns tend to follow a power-law distribution: a small percentage of investments in a given fund typically generate the majority of that fund’s total returns. That dynamic explains why funds concentrate follow-on capital on their strongest performers rather than spreading it evenly, and why a fund’s venture capital investor relations function, keeping LPs informed on portfolio performance, valuations, and expected timelines, becomes increasingly important as a fund matures and LPs look for visibility into when they can expect distributions. Firms that maintain clear, consistent investor relations practices tend to have an easier time raising their next fund from the same LP base.

What does this mean if you are raising from a VC fund?

- Ask where the fund is in its lifecycle. A fund in years one to three has more capital and time to support you through several rounds; a fund in years eight-plus is focused on exits and may have little dry powder left for new bets.

- Understand that a GP’s fund economics (fees, carry, hurdle rate) shape their incentives, not just their stated investment thesis.

- Recognize that “closed-end” does not mean inflexible: many funds retain reserves specifically for follow-on investment in their winners.

Frequently Asked Questions

How long does a typical venture capital fund last?

Most are structured with a roughly ten-year term, sometimes extended by a year or two, split between an active investment period and a longer tail focused on portfolio management, follow-ons, and exits.

What is the difference between a venture capital firm and a venture capital fund?

A firm is the overarching organization; a fund is one specific pool of capital, with its own investors and its own lifecycle, that the firm manages. A single firm can manage several funds at once.

How do venture capital funds actually make money for their investors?

Primarily through management fees (typically around 2% of committed capital annually) and carried interest (typically around 20% of profits above a minimum return threshold), paid once portfolio companies exit through an acquisition, IPO, or other liquidity event.